.webp)

You’re processing thousands of fraud insurance claims daily and watching new tricks pop up every other day. Every suspicious claim can potentially cost your company millions, while false positives frustrate legitimate customers. How do you fight against a threat that takes advantage of the rise of new technologies?

At Aloa, we develop custom AI and software solutions that help businesses like yours navigate complex challenges. Our team of engineers is made up of veterans from Google, Amazon, and we understand that implementing AI solutions requires both technical expertise and strategic vision.

This guide explores how AI is revolutionizing fraud prevention in the insurance industry, examining the technologies reshaping detection, the benefits for insurers and customers alike, real-world success stories, and what lies ahead for this critical field.

What is Insurance Fraud?

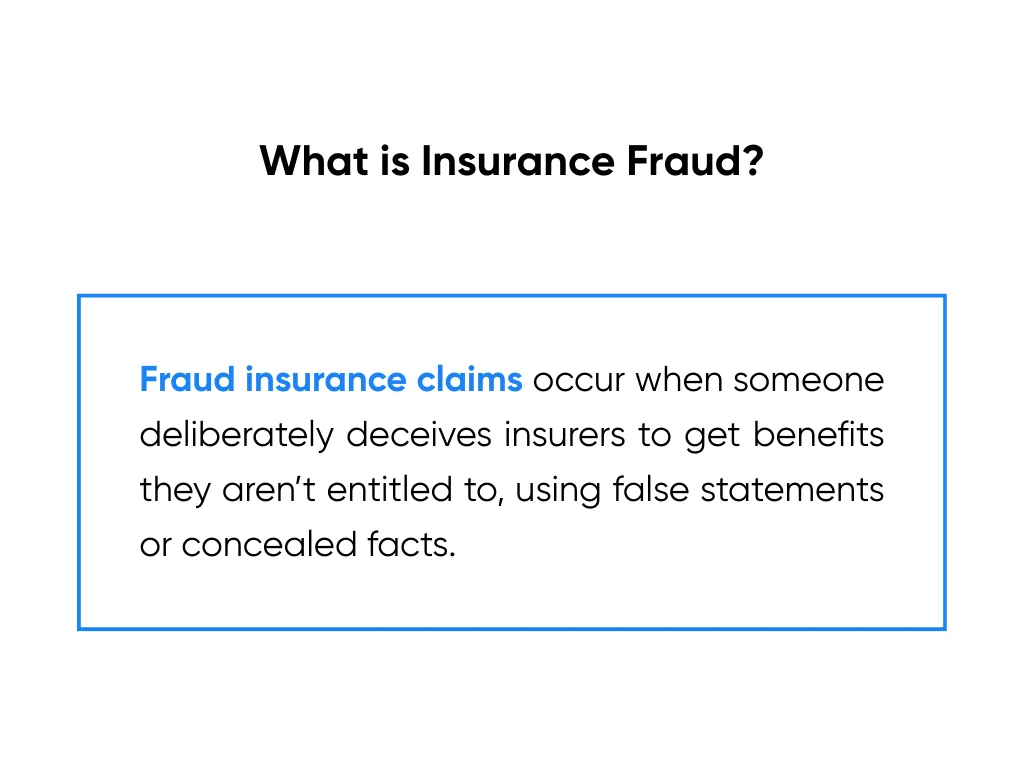

Fraud insurance claims occur when someone deliberately deceives insurers to obtain benefits or payments they're not entitled to receive. This can involve everything from false statements and concealment of facts to submitting false information (e.g. new account fraud), as long as they are made with knowing intent to defraud.

Common Types of Insurance Fraud

The various types of fraud in insurance affect multiple sectors with varying levels of sophistication. Here are some of the major ones:

- Auto Insurance Fraud: This usually takes the form of staged accident scams, often orchestrated by organized rings that deliberately cause crashes for profit. However, it can also include exaggerated injury claims from legitimate incidents or phantom vehicle damage or loss reports, when the car was actually stolen or hidden.

- Healthcare Fraud: This commonly involves billing for services never rendered and upcoding procedures to more expensive treatment codes. Healthcare providers can also sometimes perform unnecessary medical procedures solely for profit, possibly as part of a kickback arrangement between them and the patient.

- Property Insurance Fraud: This ranges from inflating the value of stolen or lost items to deliberately causing damage for claim payouts. Business owners facing bankruptcy might commit arson to collect insurance money. Contractors submitting inflated repair estimates after natural disasters is another example.

- Workers' Compensation Fraud: This includes employees faking injuries or exaggerating legitimate ones to collect benefits while working elsewhere. Employers can also commit workers’ comp fraud by underreporting payroll to reduce premiums.

The Role of AI in Fraud Detection and Prevention

AI's advancecd analytics detect fraud by cross-referencing historical data with real-time info from multiple sources. These capabilities are powered by a suite of specialized AI technologies that come together to uncover subtle anomalies that can indicate fraudulent activity.

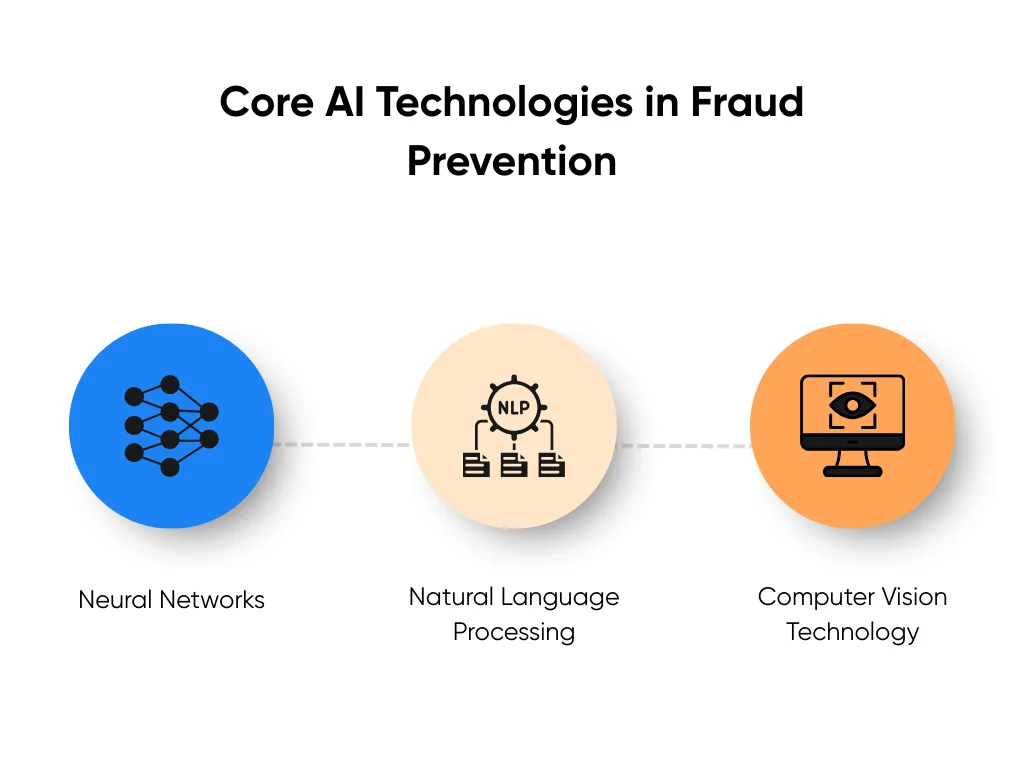

Core AI Technologies in Fraud Prevention

At the heart of fraud detection AI lies machine learning algorithms that analyze millions of data points, from claims histories and provider networks to customer behavioral patterns. Here are the main AI technologies that power those algorithms:

- Neural networks: Excel at detecting complex relationships between seemingly unrelated claims, uncovering organized fraud rings that operate across multiple insurers. These systems continuously improve their accuracy by learning from new fraud cases, adapting to evolving schemes that traditional rule-based systems would miss.

- Natural language processing (NLP): The primary tech behind generative AI, NLP analyzes unstructured data from claim descriptions, medical records, and adjuster notes to detect inconsistencies and suspicious language patterns. When someone describes their accident differently in various documents, for example, the AI notices and creates an alert for human auditors to check the anomaly.

- Computer vision technology: Verifies damage claims by comparing submitted photos against databases of legitimate damage. It can identify doctored images and assess repair costs with remarkable precision, often more accurately than human adjusters.

Anomaly Detection and Predictive Analytics

Anomaly detection systems establish baseline behaviors for legitimate claims, then flag deviations that warrant investigation. They then analyze factors including claim frequency, amount patterns, provider relationships, and temporal anomalies to identify potential fraud.

Predictive analytics takes fraud prevention a step further by forecasting fraud likelihood based on historical patterns. The models assign risk scores to claims at submission, enabling immediate routing to appropriate processing paths.

Measurable Impact on Operations

The combination of increased accuracy, processing speed, and scalability makes AI indispensable for modern fraud prevention strategies. Here’s how AI systems can deliver measurable operational improvements across the board:

- Processing Speed: Insurance company Aviva cut liability assessment time for complex cases by 23 days using AI, while achieving 30% improvement in routing accuracy and 65% reduction in customer complaints.

- Accuracy Enhancement: A 2023 study published in MDPI found that Random Forest algorithms achieve 98.21% accuracy in healthcare fraud detection with 100% recall and 98.08% precision in Saudi Arabian healthcare insurance analysis.

- Cost Reduction: ScienceSoft's analysis shows AI can reduce claim resolution costs by up to 75% and claim processing costs by 73%.

- Real-time Prevention: Deloitte's 2025 analysis states that multiple techniques including automated business rules, embedded AI, and machine learning methods can score millions of claims in real-time.

- Resource Optimization: Pilotbird's case study shows that an insurer was able to reduce claim review time from two weeks to real-time detection, achieving a 210% ROI increase in just one year and saving $5.7 million.

Implementing AI Solutions in Insurance

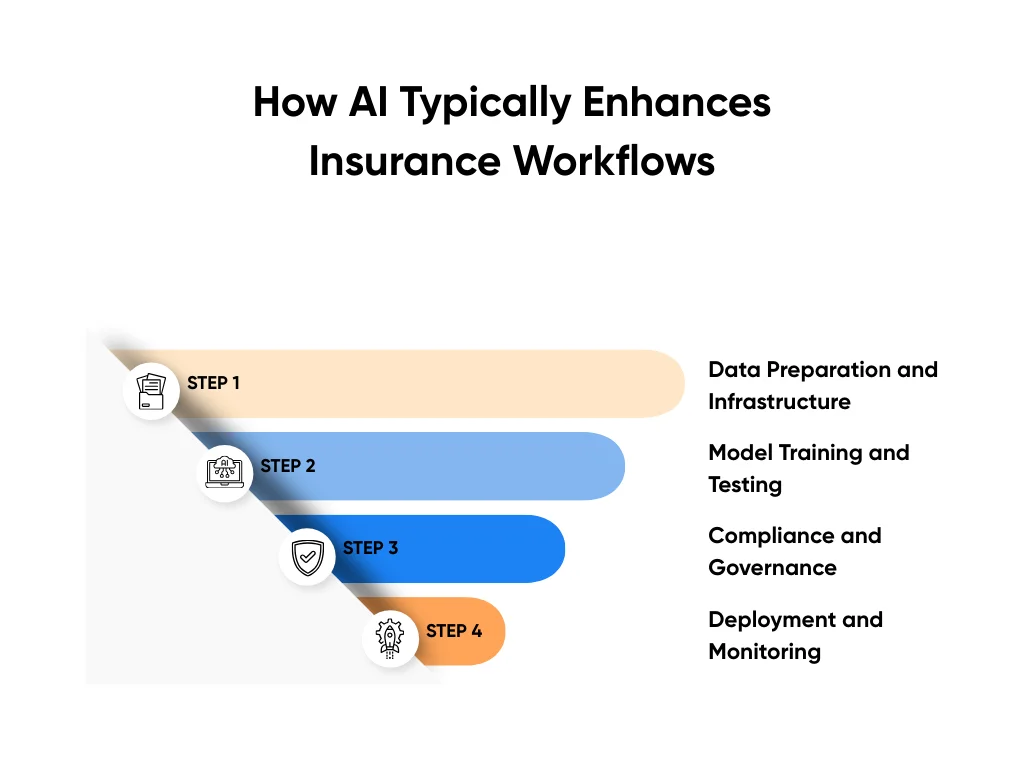

Deploying AI in insurance processes involves unique considerations specific to addressing financial crime risk. Here's how augmenting insurance workflows with AI usually goes:

Step 1: Data Preparation and Infrastructure

Integrating AI into insurance workflows starts with data collection and preparation. This involves consolidating fragmented data sources and repositories, including claims systems, policy databases, and customer records.

The consolidation phase demands careful attention to data quality and completeness to establish key fraud indicators and get meaningful results. Equally important are real-time data pipelines for instant fraud scoring, so that suspicious claims can be flagged and investigated before payments are processed. Delays can allow fraudsters to collect payouts and disappear, making recovery nearly impossible.

Step 2: Model Training and Testing

Training AI models requires historical claims data labeled as fraudulent or legitimate. Insurers typically start with supervised learning algorithms that detect known fraud patterns before advancing to unsupervised models that identify emerging schemes.

Step 3: Compliance and Governance

Regulatory compliance requires establishing AI governance frameworks that address bias, transparency, and accountability. The NAIC Model Bulletin mandates explainable AI decisions and regular bias audits. Insurers must document model development, testing protocols, and decision rationales for regulatory reviews while maintaining detailed audit trails for every automated decision.

Step 4: Deployment and Monitoring

Start with controlled pilot programs to measure detection accuracy, false positive rates, and the speed of fraud flagging. Then, you can scale across operations with API or middleware integration. Maintain effectiveness by setting up continuous monitoring for model drift, new fraud patterns, and other metrics that could be vital for retraining.

Case Studies: AI Success in Fraud Prevention

From advanced analytics and computer vision to automated red-flag systems, AI is playing a crucial role in the latest security measures implemented by financial institutions. Here’s how fraud prevention AI is delivering measurable, bottom-line results.

GEICO Turns Loss Into Profit

The Government Employees Insurance Company managed to turn a $1.9 billion underwriting loss in 2022 into a $3.6 billion profit in 2023. They did this by combining Tractable AI’s computer vision technology for instant damage assessment with CCC Smart Red Flag automated fraud detection systems that flag suspicious patterns across millions of claims across carriers. This enabled them to catch serial fraudsters who hop between insurance companies.

Shift Technology's Global Impact

Shift Technology's FORCE platform identifies over $5 billion in fraudulent claims annually for more than 100 insurance companies worldwide. Their machine learning algorithms achieve a 69% acceptance rate for fraud alerts, with 43% of investigated alerts confirming actual fraud.

Allianz's Comprehensive Business Protection

Allianz protects businesses against payment fraud, cyber fraud, and internal theft through AI that analyzes transaction patterns, vendor relationships, and behavioral indicators before losses occur. Their implementation reduced fraud losses by 30% and cut investigation time by 50% while maintaining customer satisfaction through fewer false positives and faster processing of legitimate commercial claims.

Future Trends in AI and Fraud Prevention

The next decade of AI in insurance fraud detection promises even greater disruption. New technologies like the following can be powerful enough to stop schemes before they even start:

Federated Learning

With 84% of fraud cases involving multiple industries, federated learning will enable insurers to collaborate on fraud prevention without sharing sensitive customer data. The technology allows institutions to benefit from collective intelligence while maintaining complete data sovereignty.

Quantum Computing

Set to emerge sometime in the next decade, quantum computing will enable AI to analyze thousands of risk scenarios simultaneously, identifying fraud patterns impossible to detect with classical computing.

Real-time Analytics and IoT Integration

Real-time analytics powered by edge computing will transform financial crime prevention from batch processing to instant detection:

- Telematics Data: Vehicle sensors confirm accident circumstances, speed at impact, and damage severity within seconds.

- Smart Home Sensors: Water leak detectors and security systems verify property damage claims without human intervention.

- Wearable Health Monitors: Fitness trackers and medical devices validate injury claims and treatment necessity.

- Drone Imagery: Automated aerial assessments evaluate disaster damage across entire neighborhoods within hours.

These technologies converge to create an ecosystem where AI systems can predict and prevent schemes before they materialize. According to Deloitte's analysis, these advancements could save the property and casualty insurance sector between $80-160 billion by 2032.

Key Takeaways

The use of AI is fundamentally reshaping how the financial services industry fights fraudulent activities. New developments in AI anti-fraud tools are delivering unprecedented accuracy, speed, and scalability in detecting and preventing fraud insurance claims. Millions of data points are processed in seconds, enabling the identification of even the most complex illicit user behavior in real time, foiling fraud attempts while they’re still in progress.

These advantages can clearly be seen in applications such as anomaly detection, predictive analytics, and real-time monitoring. The earlier you adopt these technologies, the sooner you can start building customer trust.

Are you seeking an ironclad defense against fraud risks? Aloa can tailor a comprehensive fraud detection system attuned to the unique aspects of your business. Our expertise in machine learning and data integration allows us to build custom AI finance software equipped with state-of-the-art fraud detection techniques. Contact us and let’s start revolutionizing your fraud prevention strategy today.

Fraud Insurance FAQs

What are the most common types of insurance fraud?

The most prevalent insurance fraud schemes include staged auto accidents where criminals deliberately cause crashes for profit. Healthcare fraud encompasses billing for services never provided, upcoding procedures to more expensive treatments, and performing unnecessary medical procedures.

How does AI improve fraud detection in insurance?

AI enhances fraud detection through machine learning algorithms that identify patterns humans cannot detect. These systems process millions of claims in real-time with up to 98% accuracy while reducing false positives by 30-50%.

What challenges do companies face when implementing AI for fraud prevention?

Primary implementation challenges include integrating AI with traditional systems that often run decades-old COBOL code. Companies must ensure data quality and completeness across fragmented systems.

How can businesses prepare for future trends in AI and fraud prevention?

Organizations should establish robust data governance frameworks now to prepare for emerging technologies. This means cleaning and organizing data, investing in cloud infrastructure for scalability, and developing partnerships with AI technology providers.